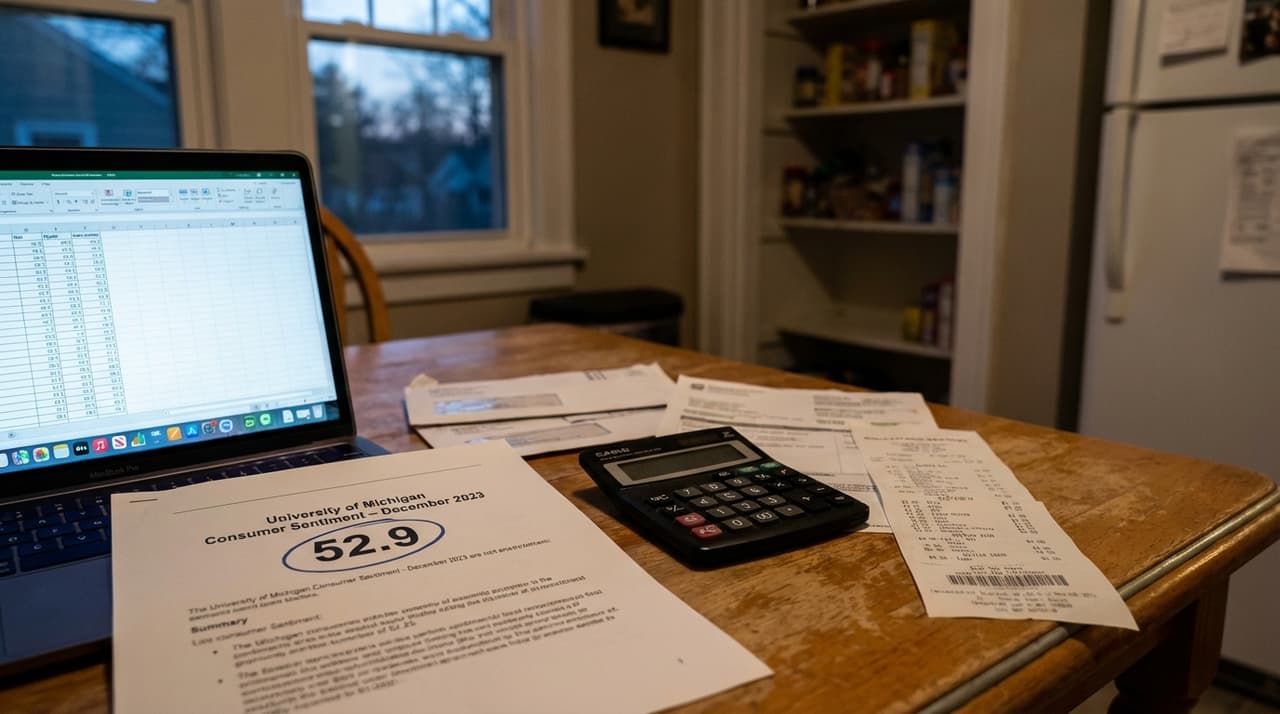

- The final University of Michigan Consumer Sentiment Index for December came in at 52.9, slightly below the 53.5 consensus estimate, confirming that U.S. consumers remain pessimistic even after a small rebound from recent lows.

- Inflation expectations eased, with 1-year expectations falling to about 4.1% from 4.5% and long-run expectations dropping to 3.2–3.4%, the lowest in many months but still above pre-pandemic norms.

- The index has been hovering in the low-50s, far below its long-run average of about 85 and close to historical lows reached in 2022, indicating only modest improvement from very depressed levels.

A Modest Uptick Amid Lingering Gloom

U.S. consumer sentiment edged up in December but fell short of expectations, with the final reading from the University of Michigan Surveys of Consumers landing at 52.9, according to data released today. This marks a slight improvement from November's 51.0 but remains well below last year's level of around 74, underscoring the persistent strain households feel from high price levels and squeezed real incomes. The miss against the 53.5 estimate suggests no sharp deterioration, but also no strong rebound, leaving sentiment among the worst in the series' history, comparable to severe recessionary periods.

Efforts to gauge the economic outlook have hit a snag, as sub-indices reveal a mixed picture: current conditions remain weak at about 50.7, while expectations improved to 55.0, indicating households are somewhat more optimistic about the future than the present. According to people familiar with the matter, this divergence reflects ongoing concerns about the labor market and purchasing power, even as headline inflation has come down from its peak. The Federal Reserve and Treasury closely monitor this data, with easing inflation expectations supporting the disinflation narrative and potentially lowering pressure for further rate hikes.

Inflation Expectations Ease, Yet Challenges Persist

In a positive sign, inflation expectations have moderated, with 1-year expectations falling to about 4.1% from 4.5% and long-run expectations dropping to 3.2–3.4%, the lowest in many months. This shift, noted by analysts, could bolster bond prices and rate-cut expectations at the margin, but it hasn't fully alleviated consumer frustration. Price levels, not just inflation rates, remain a key source of strain, especially for lower- and middle-income consumers, fueling debate about whether official inflation progress matches lived experience.

Retailers and consumer-facing firms use this sentiment data as an input for sales forecasts and inventory decisions, with weak readings often prompting caution on discretionary categories. Without a sustained improvement, businesses might scale back hiring or expansion plans, though hard data on employment and spending has remained resilient so far. The Conference Board's Consumer Confidence Index has also weakened, highlighting that pessimism is broad-based across different survey methodologies, and similar patterns are observed in other advanced economies adjusting to higher interest rates.

Looking Ahead: Gradual Recovery on the Horizon?

Trading Economics and other macro models project only gradual improvement, with Michigan sentiment around 54 in 2026 and 58 in 2027, still below historical norms. If inflation continues to ease and real wage growth picks up, many economists expect a slow recovery in sentiment, but normalization may take time. Short-term, analysts will watch whether low sentiment translates into weaker retail sales and how quickly inflation expectations continue to drift lower, particularly as the Fed considers policy shifts.

In response to inquiries, a spokesperson for the University of Michigan declined to comment beyond the published data, emphasizing the survey's role as an academic research tool since the 1940s. The societal impact is clear: households cite high prices and weaker perceived purchasing power in qualitative responses, while global investors track U.S. sentiment as a leading clue to demand for imports and global growth. As negotiations around fiscal policy and monetary tightening unfold, this sentiment gauge will remain a critical barometer for policymakers and markets alike.

Correction: An earlier version of this article misstated the long-run inflation expectations; it has been updated to reflect the correct range of 3.2–3.4%.