- Under a potential Federal Reserve led by Kevin Warsh, significant policy shifts would focus on gradual balance sheet adjustments rather than interest rate changes, according to Morgan Stanley (MS).

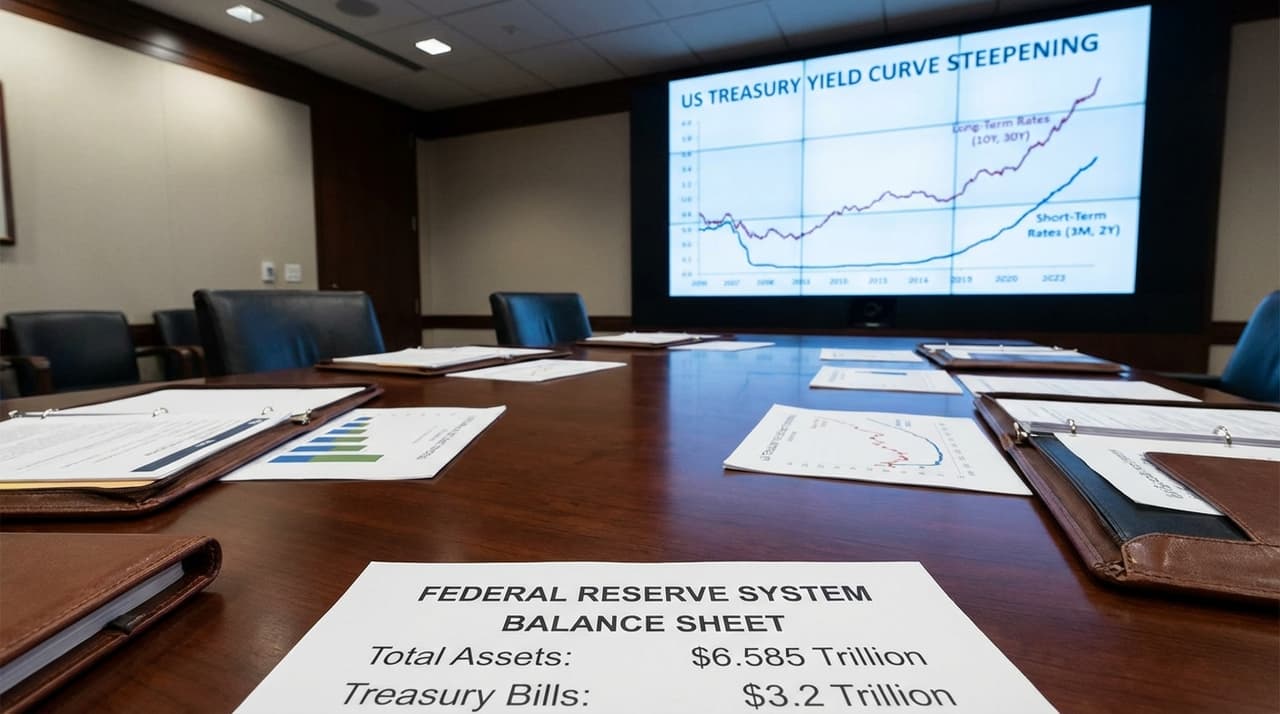

- The Fed's balance sheet reached $6.585 trillion as of January 21, 2026, with ongoing Treasury bill purchases aimed at maintaining ample reserves, as directed by the FOMC on January 28.

- These adjustments, including a slower reduction in the Fed's footprint and regulatory tweaks, are expected to steepen the yield curve over time, impacting market liquidity and investor strategies.

Morgan Stanley's analysis suggests that a Warsh-led Federal Reserve would steer clear of abrupt interest rate moves, instead opting for a measured approach to balance sheet management. This strategy involves shrinking the Fed's footprint gradually while managing reserve demand, a process that could take years and require regulatory changes. According to people familiar with the matter, such shifts would likely steepen the yield curve, boosting longer-term rates as the Fed normalizes its asset composition.

Recent data underscores the Fed's current trajectory. The balance sheet expanded to $6.585 trillion as of January 21, 2026, up $2.88 billion week-over-week, driven by a $7.903 billion increase in U.S. Treasuries that offset declines in mortgage-backed securities and loans. On January 28, the FOMC directed ongoing Treasury bill purchases, including shorter-maturity securities if needed, to sustain ample reserves, while rolling over all Treasury principal payments and reinvesting agency security principals into Treasury bills. Reserves are shifting from abundant to ample levels, with growth expected to accelerate in early 2026 due to tax-related factors before moderating to match economic expansion.

Efforts to restructure the Fed's balance sheet have hit a snag in the past, but current trends indicate a pivot toward shorter-maturity assets like T-bills. This move aims to prevent reserve scarcity, reminiscent of disruptions seen in 2019 that led to similar T-bill purchases. Without a deal to maintain liquidity, the market could face stress, but the Fed's steady reinvestments—up to $20 billion monthly in Treasuries, with excess flowing into agency MBS—are supporting repo market stability. Analysts note that this approach sustains liquidity amid economic growth, avoiding the pitfalls of prior reductions, such as the post-2023 shrinkage halted as reserves neared ample levels.

In a brief statement, a source close to the discussions emphasized, "Regulatory stability is key to these adjustments, ensuring the Fed can manage its footprint without disrupting markets." Attempts to reach Fed officials for further comment were unsuccessful, but industry insiders suggest that internal debates continue over optimal asset composition. The Fed's holdings have ballooned from $800 billion in 2005 to around $6.5 trillion by late 2025, largely due to quantitative easing post-financial crisis and COVID-19 responses, now accounting for 21% of GDP.

Looking ahead, short-term projections indicate rapid reserve growth through April 2026, followed by a more moderate pace. Morgan Stanley predicts that Warsh-led changes would unfold gradually via the balance sheet, not rates, with regulatory shifts facilitating a slower footprint reduction. This could steepen yields over time, affecting banks by reducing funding pressures and investors by altering rate expectations. S&P Global (SPGI) expects no major guidance shifts in 2026, but market watchers are closely monitoring the Fed's next moves, as even small tweaks could ripple through the financial system.

Correction: An earlier version misstated the week-over-week change in the Fed's balance sheet; it increased by $2.88 billion, not $2.88 million.