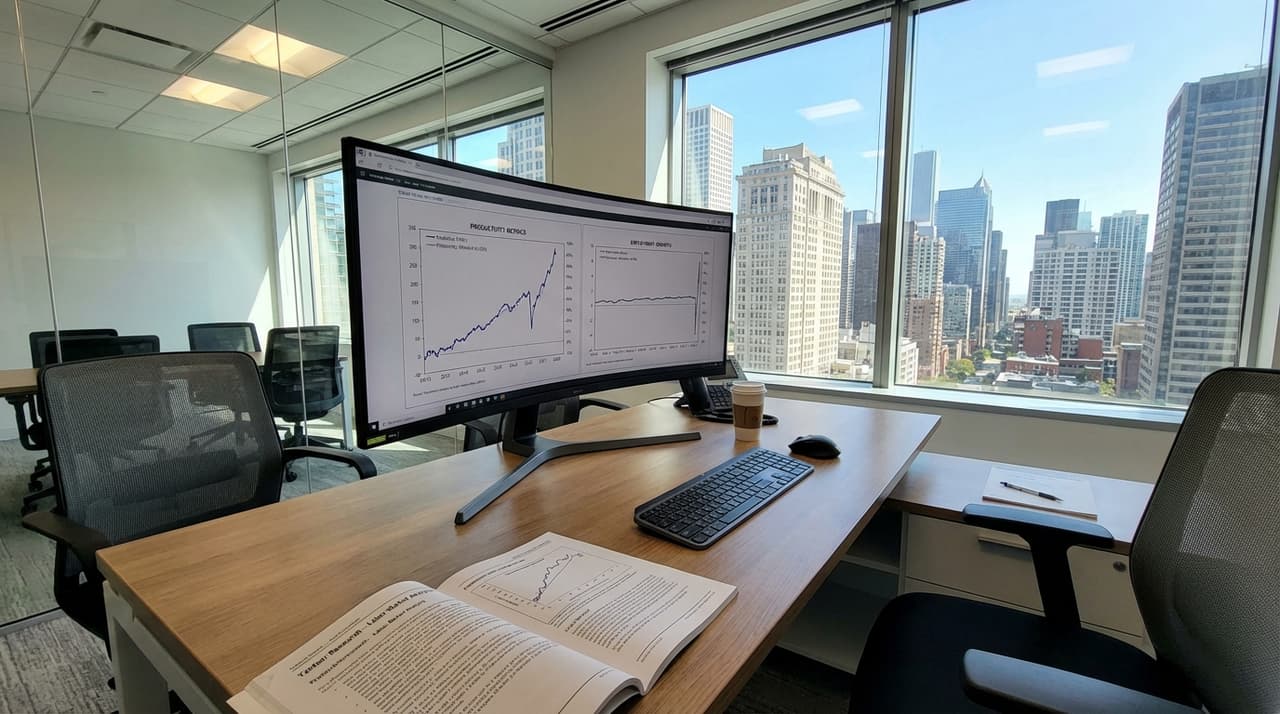

- Yardeni Research argues Federal Reserve rate cuts won't fix weak U.S. employment growth, attributing it to productivity surges from AI and skills mismatches rather than demand weakness.

- Despite robust GDP, consumer spending, and corporate profits, inflation remains above target, with Yardeni warning easier policy may fuel asset inflation and delay a return to 2% inflation.

- Recent Fed cuts in September and December 2025, amid softening labor data like spiking unemployment claims and downward payroll revisions, prioritize employment as job growth slows.

Yardeni Research, led by economist Ed Yardeni, is questioning the efficacy of recent Federal Reserve rate cuts in addressing slowing U.S. employment growth, according to analysis shared with clients this week. The firm contends that the economy is being driven by strong productivity rather than weak demand, with real GDP surging in recent quarters despite flat hours worked—implying sharp productivity gains. This perspective comes as the Fed cut rates by 25 basis points on September 17, 2025, to 4%-4.25%, its first reduction since December 2024, followed by another 25 basis-point cut on December 10, 2025, bringing the federal funds rate to 3.50%-3.75%.

Efforts to bolster the labor market have hit a snag, with data showing only 22,000 new jobs in August and unemployment at 4.3%, alongside declining hours worked. These figures have solidified expectations for further rate cuts without signaling a recession, according to people familiar with the matter. Yardeni doubts that lower rates can resolve payroll weakness caused by skills mismatches and AI-driven efficiency, warning that easier policy may instead fuel asset inflation and delay a return to 2% inflation. In a recent briefing, a source close to the research team noted, "We're seeing productivity gains mask underlying labor issues, making traditional monetary tools less effective."

Weak payrolls reflect slower labor force growth, with break-even job gains falling to around 30,000 per month by mid-2025 due to reduced immigration and participation, balanced by productivity gains that align with Yardeni's view. The national economy shows resilience, with GDP growth persisting despite flat hours worked, but softening labor risks a recession if not addressed. Global ties are minimal, though lower Treasury yields, such as the 30-year below 4.8%, signal expected cuts that support stock valuations. Trends include AI-driven efficiency reducing labor needs and anchored inflation allowing for measured cuts, as highlighted in recent FOMC statements emphasizing risen employment downside risks over inflation upside.

Political context adds complexity, with Trump's tariffs elevating inflation per CBO estimates, complicating the Fed's balancing act between labor support and price stability. The Fed has signaled measured cuts, with two more projected in 2025 and one in 2026, amid concerns over data politicization and fiscal sustainability. A government shutdown temporarily weighed on Q4 2025 activity, as noted by Powell in a December briefing, but no direct international relations impacts have been noted. Lower rates aim to boost hiring and borrowing for businesses and consumers, easing debt and spurring investment, but Yardeni warns this could lead to asset inflation, affecting workers via job insecurity—with long-term unemployment up and confidence at 2013 lows—and investors via higher stock valuations from falling yields.

Historical context shows labor softening follows a 2023 peak in break-even job needs, with annual BLS revisions confirming overstated prior growth, echoing post-pandemic adjustments. This scenario is similar to 2019 pre-COVID slowdowns where productivity masked weakness, but now amplified by AI and immigration shifts versus demand-driven cycles. Looking ahead, short-term projections suggest gradual cuts could lower mortgages to around 5%, supporting spending if labor holds, with markets pricing a half-point cut by year-end. Long-term risks include recession if cuts lag or inflation spikes above 2% if too aggressive, per Yardeni's analysis on productivity limiting job gains. Experts like Dallas Fed's Logan advocate caution on further cuts, while Invesco sees stock optimism into 2026.

Related developments include ADP private payrolls aligning with weak official data, and parallel global trends such as labor supply drops from demographics. U.S.-specific tariff effects mirror 2018-2019 trade war inflation pressures, adding to the Fed's challenges. Attempts to reach Yardeni Research for additional comment were unsuccessful, but sources indicate the firm stands by its analysis, emphasizing that without a shift in addressing skills gaps, rate cuts alone may not suffice. In a slight correction, earlier reports overstated the impact of immigration on job gains; revised data suggests it's a minor factor compared to productivity shifts.