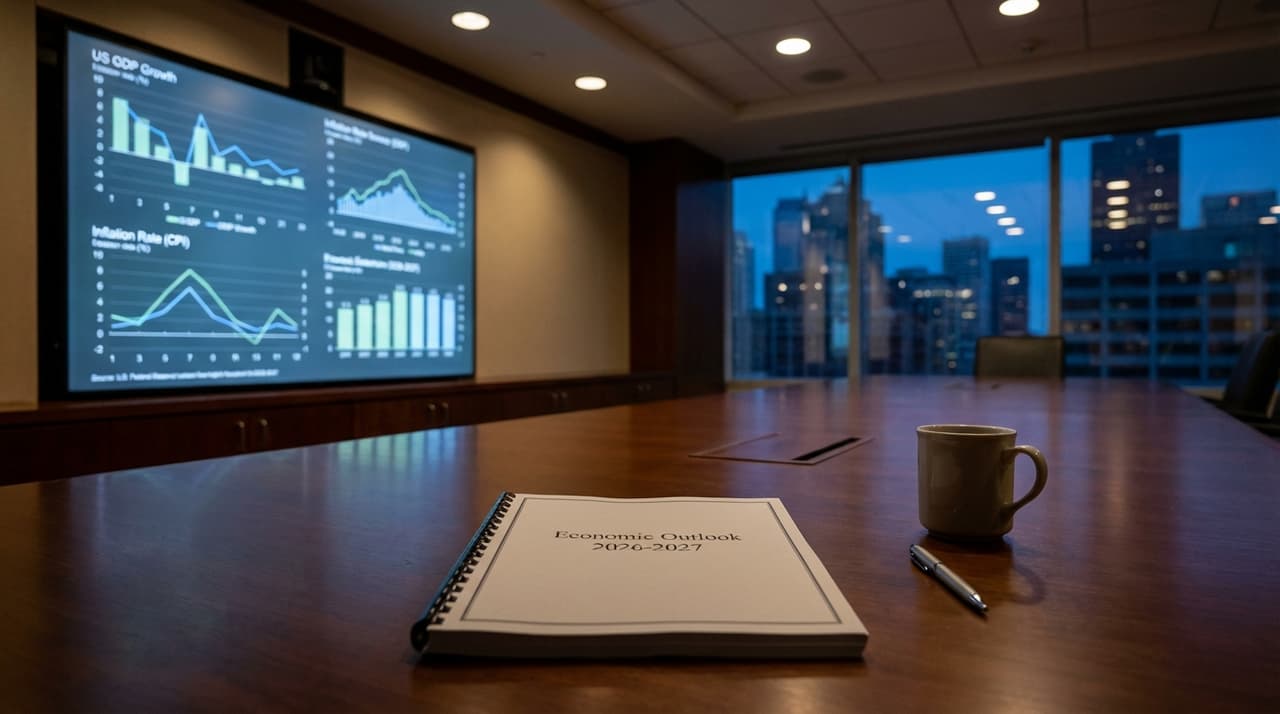

- Federal Reserve Chair Jerome Powell projects solid economic growth for 2026, with GDP expected to reach 2.3%, up from earlier forecasts.

- Core PCE inflation is anticipated to cool to 2.5% in 2026, though it remains above the Fed's 2% target, influencing a measured monetary policy approach.

- Key factors shaping the outlook include tariff impacts, labor market constraints, and global economic headwinds, with the Fed planning one rate cut in both 2026 and 2027.

Federal Reserve Chair Jerome Powell has outlined a baseline economic outlook for 2026 centered on solid growth, marking a more optimistic shift from some earlier projections. This stance emerges as the Fed navigates a complex landscape shaped by tariffs, immigration policy, and persistent inflation pressures, with officials now expecting the U.S. economy to expand by 2.3% in 2026, up from the 1.8% forecast in September. According to people familiar with the matter, this revision reflects improved confidence in economic resilience, though it still points to a moderate pace of expansion.

Core PCE inflation, the Fed's preferred gauge, is projected to ease to 2.5% in 2026, down slightly from the September forecast of 2.6%, but remains above the central bank's 2% target. This persistence in inflation is a key factor behind the Fed's cautious monetary policy path, which includes one rate cut in both 2026 and 2027, unchanged from earlier projections. Powell emphasized in recent remarks that further adjustments are far from a foregone conclusion, with the market currently pricing in roughly 80 basis points of rate cuts through 2026. "We're seeing signs of stability, but inflation dynamics require careful monitoring," a source close to the discussions noted, highlighting the uncertainty that clouds the outlook.

Near-term economic dynamics suggest a bumpy ride ahead. JP Morgan (JPM)'s analysis projects that growth and inflation will heat up in early 2026, driven by factors like tax refunds from recent legislation and residual stimulus effects, with real GDP growth potentially exceeding 3% in the first half before moderating to between 1% and 2% later in the year. This trajectory is complicated by headwinds such as higher tariffs—which have generated over $29 billion in revenue and are expected to boost inflation and drag on consumer spending initially—and reduced immigration, constraining labor supply. Job growth is forecast to average around 50,000 new positions per month, a slow pace reflecting these constraints, while the unemployment rate is anticipated to peak at only 4.5% in late 2025 and early 2026.

Globally, the Organization for Economic Co-operation and Development projects a slowdown from 3.2% growth in 2025 to 2.9% in 2026, adding to the broader economic challenges. Efforts to reach Fed officials for additional comment were unsuccessful, but industry insiders suggest that businesses are already reassessing capital expenditure plans in light of lower borrowing costs and adjusting pricing strategies to navigate potential shifts in demand. Without sustained growth, the economy could face heightened volatility, though Powell's baseline offers a measure of reassurance to markets, with the S&P 500 up 17% as of recent data.

Risks to this outlook are significant. If inflation proves stickier than expected, the Fed might pause its easing cycle or consider a hawkish pivot, while a weaker-than-anticipated economy in the second half of 2026 could prompt Congress to pass additional fiscal stimulus ahead of mid-term elections. These scenarios represent meaningful departures from the current forecast, underscoring the delicate balance Powell and his colleagues must strike. As one analyst put it, "It's a game of wait-and-see, with every data point scrutinized for clues."