- Tesla (TSLA)'s Q4 2025 revenue and non-GAAP EPS slightly exceeded analyst expectations, with shares rising 1.4% post-announcement.

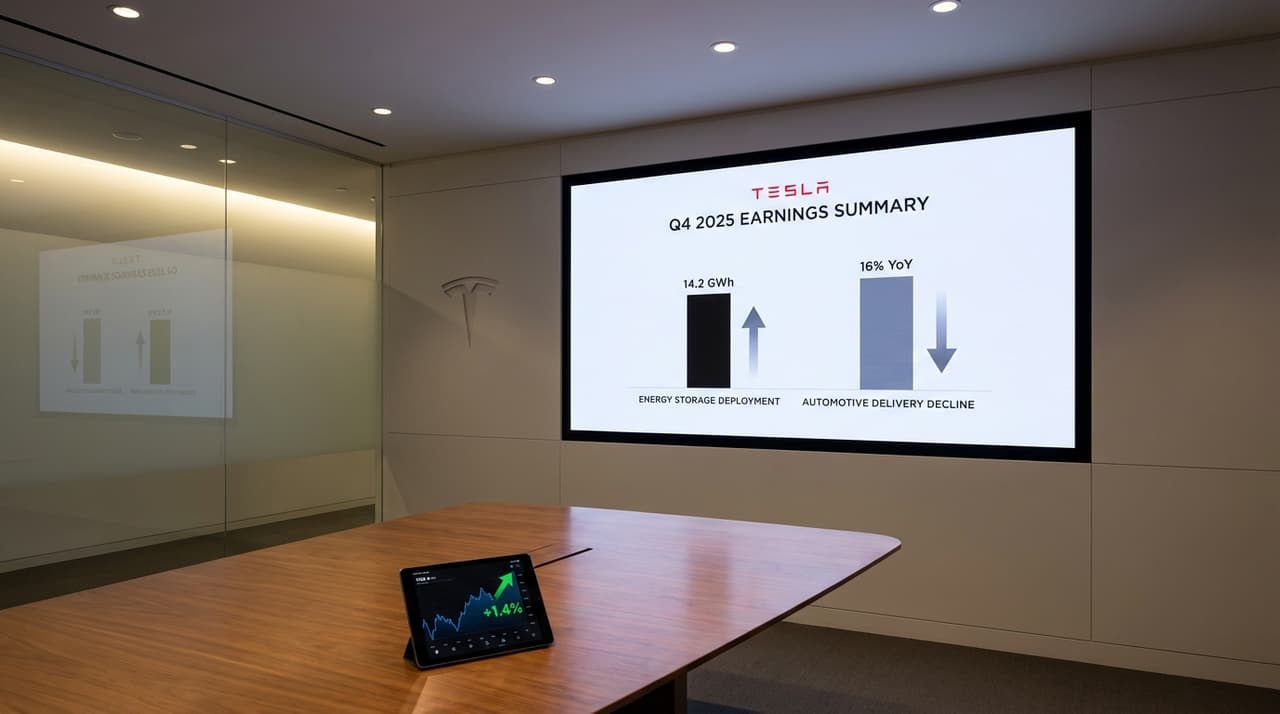

- Energy storage deployments hit a record 14.2 GWh, offsetting a 16% year-over-year decline in automotive deliveries.

- The company reported its first annual revenue drop in 2025, down 3% year-over-year, signaling a shift from hyper-growth to maturation.

Tesla's shares climbed 1.4% following the release of its Q4 2025 earnings on January 28, 2026, as the electric vehicle and clean energy giant posted a slight beat on expectations. Revenue came in at $24.901 billion, edging past the $24.766 billion forecast by analysts, while non-GAAP earnings per share reached $0.50, compared to the $0.44 consensus estimate. The modest gains reflect a mixed quarter: automotive deliveries fell to 418,227 vehicles, down 16% year-over-year, but energy storage deployments surged to a record 14.2 GWh, driving growth in that segment.

According to people familiar with the matter, the results underscore Tesla's ongoing pivot toward diversification amid softening global EV demand. "Energy storage is becoming a critical buffer as the auto market stabilizes," one source noted, pointing to the 26.6% year-over-year revenue growth in Tesla's energy business, which hit $12.8 billion for the full year. This shift comes as Tesla grapples with pricing pressures and increased competition, factors that contributed to its first annual revenue decline—down 3% to $94.8 billion in 2025—after years of rapid expansion.

In a brief statement, Tesla highlighted operational efficiency efforts and ramps in its 4680 battery and Model Y production as near-term priorities. Analysts, including those at Needham & Company who reiterated a "hold" rating post-earnings, view the company increasingly as a tech play, with long-term bets on AI and robotics like its Optimus robot and robotaxi initiatives. The disclosure of 1.1 million Full Self-Driving subscribers and progress with Neuralink's FDA updates have bolstered this narrative, even as the automotive segment faces headwinds.

Market reaction was tempered by Tesla's high price-to-earnings ratio of around 400x and the broader EV slowdown, but the energy storage record provided a silver lining. Without sustained growth in non-auto segments, the company could face heightened volatility, though current trends suggest energy demand will remain strong into 2026. Efforts to streamline costs and focus on high-margin products are underway, with insiders indicating that further updates on AI investments, including a recent $2 billion infusion into xAI, may shape future earnings calls.

Correction: An earlier version misstated the non-GAAP EPS figure; it has been updated to $0.50.