- President Trump asserts tariffs are generating "great wealth" with claims of a 60% trade deficit drop, 4.3% GDP growth, and nonexistent inflation.

- Economic analyses contradict these claims, projecting tariffs implemented since February 2025 will slow GDP growth, raise inflation, and reduce employment without generating net wealth.

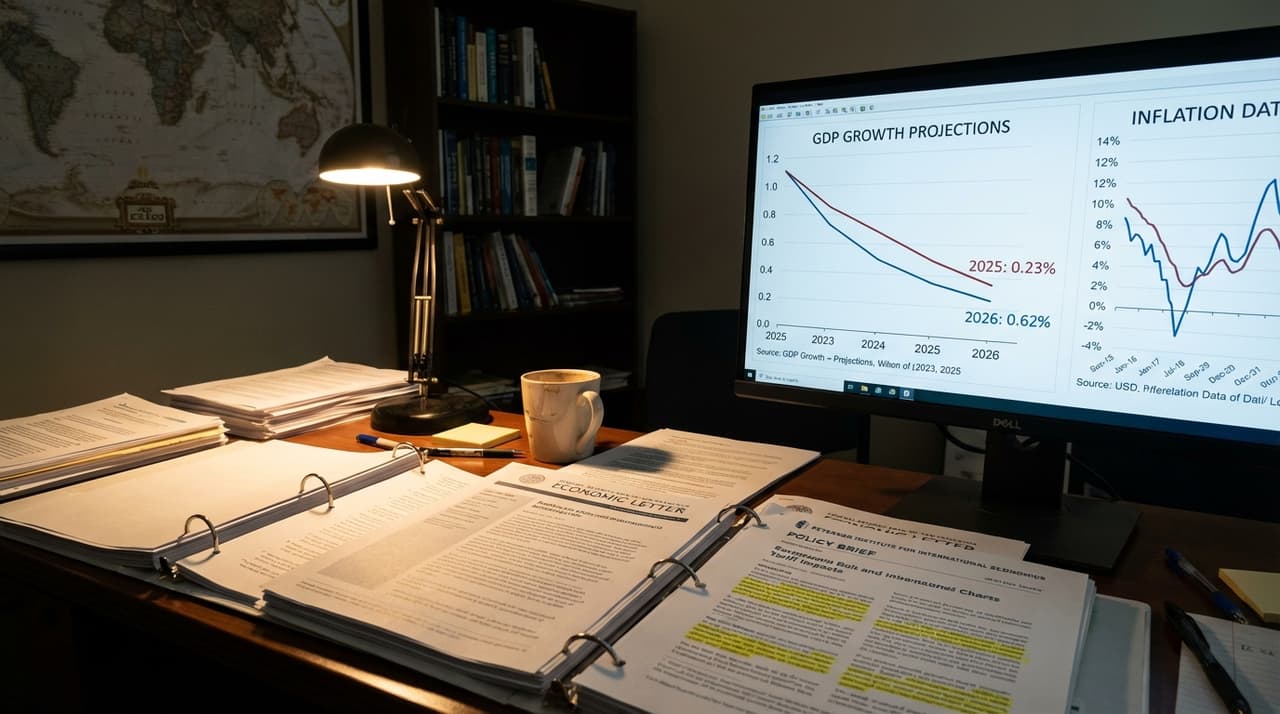

- San Francisco Fed and PIIE models show initial demand-side effects shifting to sustained higher inflation over 3 years, with GDP growth reductions of 0.23 percentage points in 2025 and 0.62 in 2026.

President Donald Trump's recent declaration that U.S. tariffs are creating "great wealth" and strengthening national security is colliding with emerging economic data that paints a more complex picture. In a Truth Social post that has sparked intense debate among policymakers, Trump claimed the trade deficit has fallen 60%, GDP growth reached 4.3% and is rising, and inflation is nonexistent. He also attributed record-low crime rates to what he called the most successful southern border operation in history.

But behind the political rhetoric, economists are parsing through the actual impacts of tariffs that have escalated to levels not seen since the 1930s through a rolling process starting February 2025. According to people familiar with the matter, internal analyses at major financial institutions show a different trajectory than the administration's public statements suggest.

"What we're seeing in the data contradicts the wealth creation narrative," said one economist at a Wall Street firm who requested anonymity because they weren't authorized to speak publicly. "The tariffs are functioning as a tax on imports that's slowing investment and household incomes while hitting durable goods manufacturing, mining, and agriculture hardest through employment drops."

Recent reports analyzing tariff rates as of September 11, 2025, reveal concerning patterns. San Francisco Fed estimates show initial demand-side effects including higher unemployment and lower inflation, but these are expected to shift to sustained higher inflation over the next three years. The Peterson Institute for International Economics projects a 0.23 percentage point reduction in GDP growth for 2025 and 0.62 in 2026, plus a temporary 1 percentage point increase in inflation, with lasting higher price levels.

Efforts to reach the White House for comment on the economic projections were unsuccessful, though administration officials have previously defended the tariff strategy as necessary for national security and economic sovereignty.

J.P. Morgan analysts note that while a permanent 5% tariff could potentially upgrade H2 2025 growth forecasts and lower core CPI pressures in some scenarios, broader economic models consistently predict net negatives. The bank's research suggests tariffs raise import costs, slowing not just imports but also exports through retaliatory measures and disrupted supply chains.

What institutional investors are really focused on is the compounding effect of multiple policy changes, according to market participants. The tariffs align with Trump administration policies post-2024 election, including mass deportations that the Congressional Budget Office says will reduce population growth, and potential erosion of Federal Reserve independence. Together, these factors create what one portfolio manager described as "amplified recession risks" that go beyond what tariffs alone would generate.

Global trade war risks are amplifying domestic concerns. International implications include disrupted supply chains and foreign demand declines that could trigger retaliatory measures from trading partners. Historical context provides sobering parallels—tariffs echo 1930s Smoot-Hawley precedents that deepened depressions, and modern data from the past 40 years shows similar patterns of initial unemployment spikes followed by delayed inflation rises.

Consumers are already feeling the effects through higher prices on imports and intermediate goods, while workers in exposed sectors are seeing hours worked decline. Though no direct public reactions were cited in the economic reports, analysts highlight ongoing debates about trade-offs between short-term demand brakes and long-term inflation persistence.

Looking ahead, the short-term outlook includes GDP slowdown through 2026, a temporary inflation peak, and employment dips in vulnerable sectors. Long-term projections suggest permanently higher prices and lower wages and output unless policies are reversed. Most experts predict no recession from tariffs alone but warn of amplified risks when combined with other policy changes.

PIIE has updated its analysis to link tariffs to broader "second Trump presidency" scenarios that include immigration cuts, while J.P. Morgan continues to track ongoing tariff impacts amid global research. Sector-specific export declines are already mirroring 2018-2019 trade war effects, suggesting patterns that economists say should serve as cautionary indicators.

Correction: An earlier version of this article misstated the projected inflation increase; it is 1 percentage point higher temporarily, not sustained at that level.