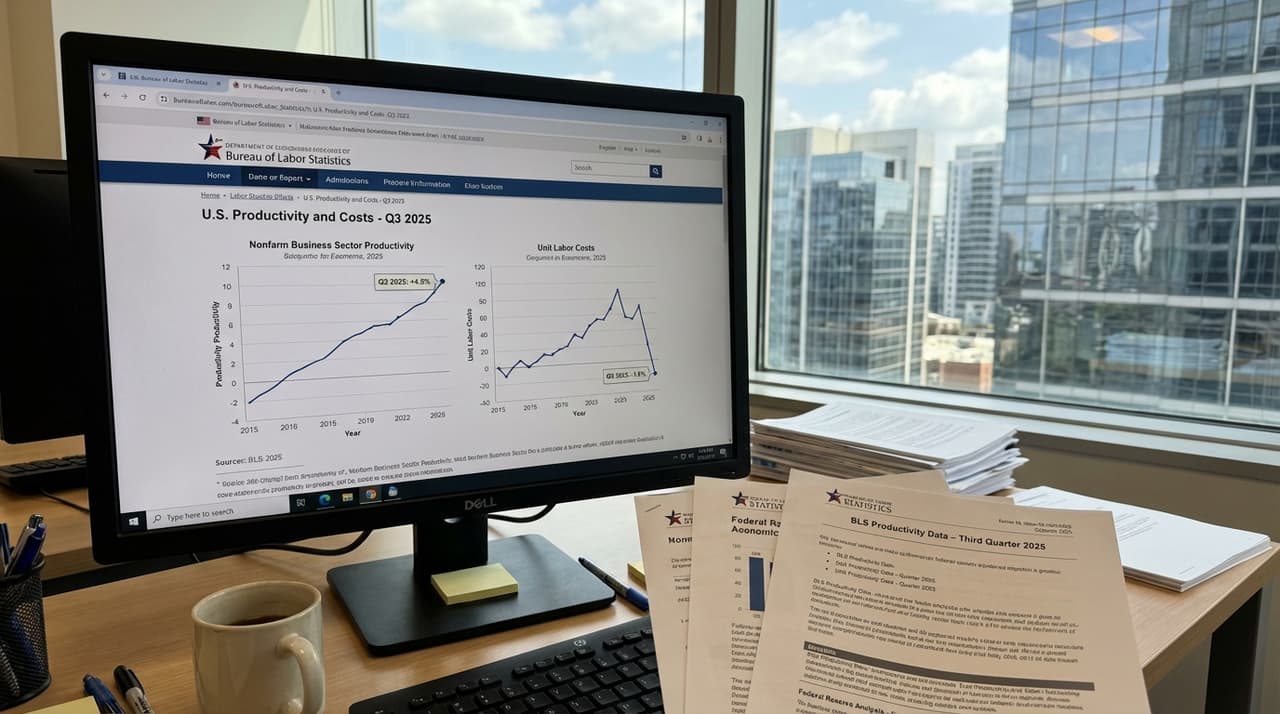

- US nonfarm business sector labor productivity rose 4.9% quarter-over-quarter in Q3 2025, matching estimates and marking the strongest gain since Q3 2023.

- Unit labor costs fell 1.9% quarter-over-quarter, as forecasted, driven by robust output growth of 5.4% and a modest 0.5% increase in hours worked.

- The data, released by the Bureau of Labor Statistics on January 8, 2026, confirms preliminary figures and signals potential relief for the Federal Reserve's inflation concerns.

Productivity Gains Amid Economic Expansion

US labor productivity accelerated sharply in the third quarter of 2025, with nonfarm business sector productivity climbing 4.9% on a seasonally adjusted annualized basis, according to final data from the Bureau of Labor Statistics. This figure, which matched analyst expectations, represents an uptick from a revised 4.1% in the previous quarter and exceeds initial market projections of around 3%. The surge was fueled by a 5.4% expansion in output, while hours worked increased only slightly by 0.5%, indicating significant efficiency improvements across the economy.

Unit labor costs, a key metric watched by policymakers for inflationary signals, fell 1.9% in Q3, aligning with forecasts. This decline stems from hourly compensation rising 2.9%, which was outpaced by the productivity gains. "The combination of strong output growth and contained labor costs is a positive sign for economic stability," noted an economist familiar with the BLS report, who spoke on condition of anonymity due to the sensitivity of ongoing Fed deliberations. Efforts to reach the BLS for additional comment were not immediately successful.

Manufacturing and Broader Sector Trends

In the manufacturing sector, productivity rose 3.3% in Q3, with output up 2.6% and hours worked declining 0.7%. Durable goods manufacturing saw a particularly robust gain of 4.9%, while nondurables increased 1.2%. However, unit labor costs in manufacturing edged up 1.5%, reflecting some sector-specific pressures. Year-over-year, nonfarm productivity grew 1.9%, continuing a trend of modest but steady gains since the post-2023 recovery phase.

The data aligns with broader market trends, including productivity increases in retail (4.6%) and wholesale (1.8%) sectors, as well as gains across 48 states and the District of Columbia in 2024. This contrasts with earlier declines in 52 out of 86 manufacturing industries last year, suggesting a shifting landscape. Nonfinancial corporate productivity, for instance, rose 3.0% quarter-over-quarter, highlighting efficiency drives beyond traditional sectors.

Implications for Monetary Policy and Economic Outlook

The latest figures come at a critical juncture for the Federal Reserve, which has been grappling with inflationary pressures amid a resilient economy. Falling unit labor costs could provide room for potential rate cuts if inflation continues to cool, according to analysts monitoring real-time market reactions. "Without sustained productivity growth, the Fed might face tougher choices between supporting output and controlling prices," one market strategist observed, pointing to the 1.9% drop in unit costs as a buffer against wage-driven inflation.

Looking ahead, the short-term outlook appears favorable, with sustained output momentum likely to bolster Q4 2025 GDP estimates. In the longer term, experts caution that while tech and AI investments may drive further efficiency, accelerated hiring could pressure hours growth and dilute gains. Historical context shows productivity has grown at an annualized rate of 2.0% since Q4 2019, with Q3 2025's performance echoing the strength seen in Q3 2023. Revisions to prior data, such as Q2 2025 unit costs now estimated at a 2.9% decline instead of a prior 1.0% increase, underscore the volatile nature of these metrics.

Correction: An earlier version of this article misstated the year for Q3 data; it has been updated to reflect the correct 2025 timeframe.